Events & Webinars

The iPhone Moment for Money: Why Stablecoins Need Better Taps, Not Just Better Pipes

/ Thought Leadership

Published May 5, 2026

Written by Alistair Rennie

◻️ Drawing on new Protocol Theory research across Australia, the UK, and the US, Alistair Rennie argues that stablecoins’ “iPhone moment” will come when programmable money moves beyond infrastructure and solves real consumer problems through safer, smarter, and more useful financial experiences.

Stablecoins need better taps, not better pipes

Stablecoins have become one of the clearest examples of product-market fit in digital assets.

They move value quickly. They can reduce cost. They operate continuously. They can settle across borders without relying on the same institutional architecture as traditional payment systems. For businesses, platforms, and financial institutions, the supply-side benefits are increasingly well understood.

But if stablecoins are going to become part of everyday financial life, the industry needs to spend more time on a different question:

What do people actually want to do with them?

That question defines the next phase of stablecoin innovation.

For years, much of the industry conversation has focused on the “pipes”: issuance, liquidity, settlement, reserves, compliance, interoperability, and infrastructure. These things matter. They are foundational. They are also only one side of the adoption equation.

The next battle will happen at the “taps”—the interfaces, products, agents, apps, wallets, services, and embedded experiences through which people and businesses actually encounter programmable money.

The history of technology adoption suggests that infrastructure becomes transformative when the demand layer catches up. The internet created the conditions for digital commerce, search, streaming, and social platforms. But it was the iPhone that made those services accessible, habitual, and part of daily life.

Stablecoins may be approaching a similar moment.

The question is whether the industry can move from better rails to better experiences.

◼️ Watch the keynote: This article expands on the argument Alistair Rennie presented at Consensus Miami 2026, where he challenged the idea that faster and cheaper payments alone will drive mainstream stablecoin adoption. Watch the full keynote here.

Faster and cheaper will not be enough

The standard case for stablecoins often begins with efficiency.

Stablecoins can enable faster settlement. They can reduce fees. They can support 24/7 liquidity. They can make cross-border payments more efficient. For businesses, especially those dealing with treasury movement, remittances, settlement risk, or international money flows, these advantages are significant.

But consumer behavior rarely changes on efficiency alone.

In new Protocol Theory research conducted in April 2026 among 3,023 adults aged 18 to 65 across Australia, the United Kingdom, and the United States, we found that many people already understand the limitations of existing payment systems: 57% of adults agree that card payments involve fees, whether they see those fees directly or not, while 67% understand that card transactions can take a few days to fully settle and be reflected in their final bank balance.

Yet people keep using cards.

That finding matters. It suggests that awareness of inefficiency does not automatically create behavior change. Consumers are already making trade-offs: they tolerate settlement delays and hidden payment costs because cards offer convenience, acceptance, protection, habit, rewards, and familiarity.

In the same research, 56% of adults said they value the convenience, protection, and features of cards more than the time it takes for their bank balance to fully update.

That is the limitation of treating faster and cheaper as the whole story. It describes what stablecoins improve in the system. It does not fully explain what would make people adopt and habitually use them.

The needs are real, but they are unevenly distributed

Payment pain is not universal. It concentrates among people with more sophisticated, demanding, or financially exposed behaviors.

Our research identified several cohorts with higher exposure to digital money, payment complexity, or financial pressure. These included stablecoin users, Gen Z adults, users of digital wallets or payment apps, heavy AI users, and people reliant on regular cross-border payments.

Among all adults, 31% say settlement time is a real problem. Among stablecoin users, that rises to 59%. Among remittance-reliant consumers, it rises to 61%. Among heavy AI users, it is 55%.

That does not mean settlement speed is irrelevant. It means the value of settlement speed is segment-dependent. For people who rarely move money across borders, rarely manage complex financial flows, and rarely experience cashflow pressure, settlement delays may be an irritation rather than a trigger for switching. For people dealing with remittances, multiple apps, unstable cashflow, digital assets, or more complex financial behavior, settlement becomes much more salient.

This is where stablecoin strategy needs more precision.

The early demand for programmable money is likely to come from people with higher financial complexity, higher digital sophistication, or sharper pain points. Over time, those use cases can become simpler, more embedded, and more mainstream.

That is usually how adoption works. Start where the pain is sharpest. Prove the utility. Then simplify the experience until the value becomes obvious to broader markets.

The product has to solve a real problem

One of the most important findings in the research was behavioral.

When it comes to financial choices, most consumers are not trying to optimize every decision. Asked whether they typically compare every available option to find the best one, or choose something good enough to meet their needs, 70% of adults were “satisficers.” Only 30% were “maximisers.”

That distinction matters for stablecoins.

Maximisers may respond to lower fees, faster settlement, better yield, or technical superiority. They compare. They optimize. They are more likely to notice marginal improvements.

The mass market behaves differently. Most people choose what works well enough, with acceptable effort, acceptable risk, and acceptable familiarity.

So stablecoin applications need to pass a different behavioral test. They need to make people’s lives easier, safer, more controlled, or more rewarding in ways that feel immediate.

Our research found that 56% of adults want to spend less time managing admin and more time enjoying life. 42% feel overwhelmed by the number of purchase options. 41% find it mentally draining to track renewals. 39% say they do not have time for proper budgeting. 38% say they have too many loyalty cards.

These are everyday problems, and they point to a larger opportunity for programmable money.

Programmable money needs to become practical utility

Programmability is where stablecoins can become more than a faster payment instrument.

Money can follow rules. It can respond to conditions. It can move when a verified event happens. It can be restricted, released, split, streamed, paused, protected, or delegated. It can interact with wallets, merchants, loyalty systems, AI agents, identity layers, escrow mechanisms, and smart contracts.

That creates a different kind of value proposition.

Imagine money that automatically helps a household budget around incoming salary and recurring expenses. Money that pays utility bills as usage occurs. Money that prevents a child’s allowance from being spent outside parent-defined categories. Money that releases funds only when delivery is verified. Money that consolidates loyalty rewards and applies them intelligently at checkout. Money that protects an AI agent from spending outside pre-set rules.

These are the kinds of use cases we tested in the research.

The strongest mass-market concept was anti-fraud programming, with 50% of adults saying they would be very or extremely likely to switch to a trusted provider offering the service. Programmable parent money followed at 42%, smart travel insurance at 41%, programmable loyalty rewards at 39%, and verified delivery or escrow at 36%.

The pattern is revealing. The leading use cases are not primarily about settlement speed. They are about security, control, optimization, and empowerment.

This gives the industry a stronger demand-side frame.

The lesson is simple: the strongest consumer opportunities are not just about moving money more efficiently. They are about making money safer, smarter, and more useful.

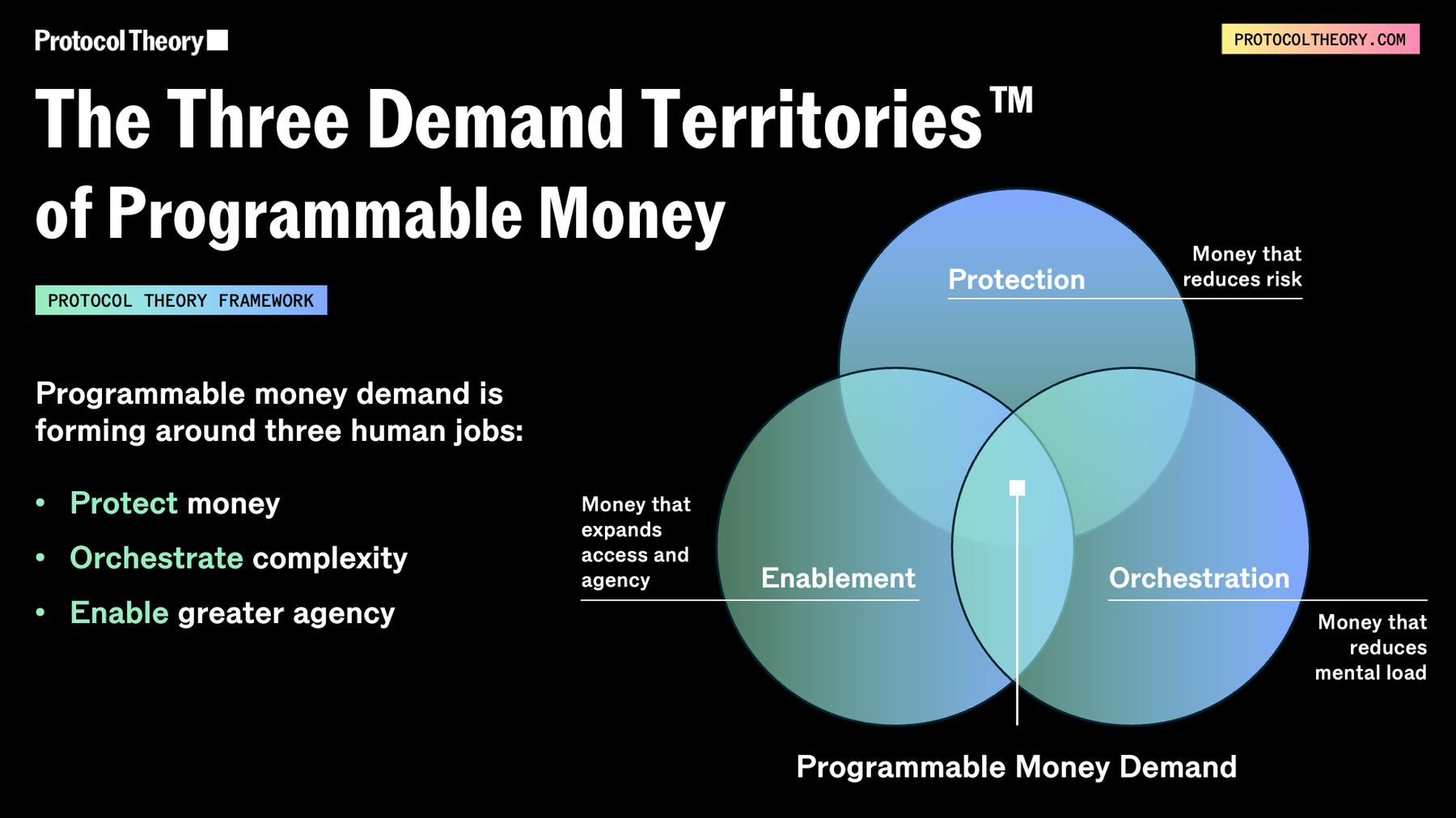

Protocol Theory’s Three Demand Territories for Programmable Money

At Protocol Theory, we see programmable money demand organizing around three core territories: Protection, Orchestration, and Enablement. Together, these define the consumer jobs that programmable money must perform to move from technical capability to everyday utility.

They also provide a more useful strategic lens than “payments efficiency” alone.

1. Protection: money that reduces risk

Protection is the clearest mass-market demand territory.

Consumers do not simply want money to move faster. They want money to move safely. They want protection from scams, fraud, failed delivery, overspending, poor agent decisions, accidental renewals, and financial mistakes.

This is why anti-fraud programming ranked as the strongest use case in our research. 50% of adults said they would be very or extremely likely to switch to a trusted provider offering it.

Protection also explains the appeal of verified delivery, smart travel insurance, subscription controls, and AI agent safeguards. Each use case gives users more confidence that money will only move under the right conditions.

The strategic lesson is straightforward: for many consumers, programmable money becomes compelling when it acts as a safety layer.

2. Orchestration: money that reduces mental load

Orchestration is about making financial life easier to manage.

Modern consumers are surrounded by recurring payments, loyalty programs, app-based purchases, subscriptions, bills, wallet balances, card options, rewards schemes, and financial decisions. The problem is not only payment speed. It is coordination.

Programmable money can help by organizing financial actions around rules, timing, context, and user intent.

This is the demand logic behind auto-budgeting, live utility payments, subscription managers, loyalty optimization, income streaming, and travel-related automation. These concepts are valuable because they reduce admin, simplify decisions, and help money work in the background.

In our research, 56% of adults said they want to spend less time managing admin and more time enjoying life. That is the behavioral foundation of Orchestration.

The strategic lesson: programmable money becomes more useful when it manages complexity for the user.

3. Enablement: money that expands access and agency

Enablement is about helping people do things they currently find difficult, constrained, or unavailable.

This includes programmable parent money, credit building, live income streaming, micro-task rewards, agentic remittance, and wealth-building tools. These are use cases where programmable money can give people more control, flexibility, access, or financial capability.

For some users, Enablement may mean helping children learn financial responsibility. For others, it may mean building credit, receiving income sooner, earning through digital tasks, sending money across borders more intelligently, or using AI agents without surrendering control.

This territory is especially important for higher-need and more digitally sophisticated cohorts. In the research, switching propensity across many programmable money concepts was materially higher among stablecoin users, heavy AI users, and remittance-reliant consumers.

The strategic lesson: programmable money can become a capability layer, not only a transaction layer.

Together, these territories suggest that the future of stablecoin adoption may depend less on “crypto payments” as a standalone category and more on programmable financial services that happen to use stablecoins underneath.

That distinction matters commercially. Consumers do not need to care about the rail. They need to care about the outcome.

The strongest use cases move customers, not just money

Across the concepts we tested, the clearest demand signals came from use cases that performed one or more of these jobs:

- Protect the user.

- Orchestrate complexity.

- Enable greater control, access, or agency.

That is the real demand-side opportunity.

Stablecoins become interesting to consumers when they help people avoid bad outcomes, reduce mental load, make better decisions, protect money, and automate useful financial tasks.

They become commercially powerful when those benefits are delivered by trusted providers through simple experiences.

The stronger signals among advanced cohorts are even more instructive.

Anti-fraud programming rises from 50% among all adults to 61% among stablecoin users, 70% among heavy AI users, and 72% among remittance-reliant consumers.

Programmable parent money rises from 42% among all adults to 69% among heavy AI users and 73% among remittance-reliant consumers.

Smart travel insurance rises from 41% among all adults to 59% among stablecoin users, 67% among heavy AI users, and 71% among remittance-reliant consumers.

The commercial implication is clear: build for sharp pain first, then scale through simplicity.

◼️ Download the research summary: For a concise view of the data behind these findings, download Protocol Theory’s one-page summary 'Top 10 Programmable Money Use Cases'. The summary ranks the use cases most likely to drive provider switching and highlights three key findings for payment providers, wallets, fintechs, and stablecoin platforms.

Agentic commerce needs safeguards and gradual trust

The rise of AI agents adds another layer to the stablecoin opportunity.

If agents are going to research, recommend, negotiate, purchase, renew, cancel, book, or optimize on behalf of users, they will need a way to interact with money. Stablecoins could become a natural transaction layer for agentic commerce because they are programmable, digital, and interoperable.

But autonomy is a sensitive issue.

Our research found that 44% of adults reject agentic commerce outright, at least in its current framing. Only 3% of adults are ready for fully autonomous agentic commerce. A further 5% are open to autonomy with alerts, while 9% prefer semi-autonomous behavior with strict guidelines and prompting.

Among stablecoin users and heavy AI users, openness is materially higher, but even these groups tend to prefer staged involvement. Many are comfortable with research-only or research-with-final-approval models before moving toward greater autonomy.

This points to an important design principle: agentic commerce needs trust architecture.

People will need rules, permissions, caps, alerts, approvals, category restrictions, merchant restrictions, audit trails, and easy override controls. They will also need confidence that an agent cannot make costly mistakes with their money.

That is why the AI Agent Safeguard concept is strategically important. It positions programmable money as a control layer for AI spending.

Among all adults, 28% said they would be very or extremely likely to switch to a trusted provider offering this kind of safeguard. Among stablecoin users, that rises to 57%. Among remittance-reliant consumers, it rises to 60%. Among heavy AI users, it rises to 62%.

The near-term opportunity in agentic commerce may be safe delegation.

Give users control first. Let autonomy follow trust.

The next stablecoin winners may be demand-layer companies

The most valuable technology companies in the world did not succeed only because supply-side infrastructure improved. They succeeded because they controlled demand. They created interfaces, marketplaces, apps, defaults, habits, and ecosystems that shaped how people accessed digital life.

That lesson should matter for stablecoins.

The industry has invested heavily in the pipes. That work has been necessary. But the next phase of value creation may come from the taps: the wallets, apps, agents, merchant tools, financial services, loyalty platforms, remittance products, and embedded experiences that turn stablecoins into useful behavior.

This creates a clear strategic challenge for builders.

Do not only ask whether a stablecoin product is faster, cheaper, or technically superior. Ask what job it performs in a user’s life. Ask whether it protects them, orchestrates complexity, or enables something they could not easily do before. And ask whether the experience is trusted enough and simple enough for people who are not trying to optimize every transaction.

The iPhone moment for money will come when programmable money becomes useful enough that people choose it without needing to understand the pipes underneath.

◼️ Watch Alistair Rennie explain the argument at Consensus Miami 2026

In this keynote, Alistair explains why lower fees and faster settlement are unlikely to be enough by themselves, and why stablecoin adoption will depend on programmable utility, trusted interfaces, and real-world use cases.

Build for demand, not just infrastructure

Stablecoins are entering a new phase of competition. The next winners will be the companies that understand where demand is forming, which use cases create real switching intent, and how programmable money can solve practical problems in everyday financial life.

At Protocol Theory, we help organisations operating at the edge of finance, technology, and digital markets understand the human intelligence behind growth: what people need, what they trust, what they choose, and what will move markets next.

If your team is building the next generation of stablecoin, wallet, payment, or agentic finance products, Protocol Theory can help identify where demand is forming, which use cases create switching intent, and how to turn programmable money into products people actually choose. ◼️

Sign up to receive Protocol Theory’s latest research on programmable money, agentic stablecoins, and the demand-side future of consumer finance.

About the author

Alistair Rennie

Global Head of Innovation & Thought Leadership

Alistair Rennie is Global Head of Innovation & Thought Leadership at Protocol Theory. Formerly a Research Lead at Google, he was lead author of the landmark “Messy Middle” report on consumer decision-making. With over 25 years’ experience in consumer insight, strategy, and innovation, Alistair now helps Web3 brands generate fresh perspectives on existing challenges to help drive new growth.

Related articles

Events & Webinars

Industry Insights