Events & Webinars

The Crypto Borrowing Gap: Why Crypto-Backed Lending Needs Confidence, Not Just Demand

/ Reports & Whitepapers

Published May 21, 2026

Written by Protocol Theory

◻️ New research commissioned by Ledn and conducted by Protocol Theory shows that crypto-backed lending has a demand problem hiding in plain sight: crypto holders are open to borrowing, but providers must first earn the confidence needed to convert interest into adoption.

Crypto has become a major global asset class. It is held by millions of people, increasingly recognised by institutions, and progressively integrated into mainstream financial portfolios.

Yet one part of the market remains comparatively underdeveloped: borrowing against crypto.

In traditional finance, borrowing against long-term assets is a familiar behaviour. Homeowners borrow against property. Investors borrow against securities. Businesses borrow against assets, receivables, and cash flows.

The logic is simple: people often want access to liquidity without selling an asset they intend to keep.

Crypto has the same potential. But it has not yet reached the same level of behavioural normality.

New research commissioned by Ledn and conducted by Protocol Theory suggests the issue is not a lack of interest. It is a lack of confidence.

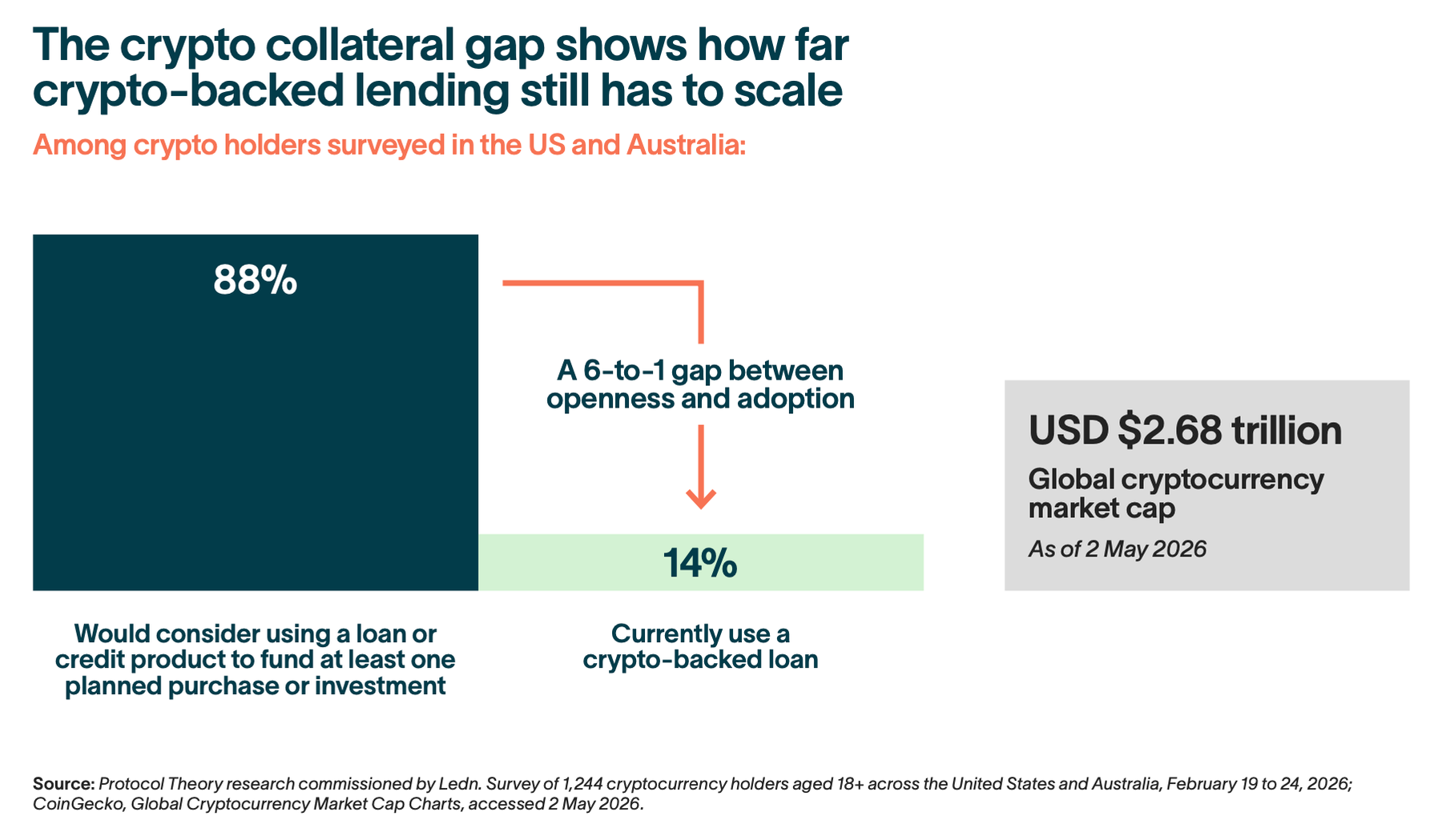

Among crypto holders surveyed in the United States and Australia, 88% said they would consider using a loan or credit product to fund at least one planned purchase or investment. Yet only 14% currently use a crypto-backed loan.

This is what Ledn and Protocol Theory describe as the crypto collateral gap: the distance between the scale of crypto ownership and the much smaller adoption of collateralised borrowing against digital assets.

◼️ You can read Ledn’s original post on the research here, or download the full report below:

Crypto lending’s confidence challenge

The findings point to an important distinction for the future of crypto-backed lending.

Many crypto holders already understand the broad value proposition. They can see why borrowing against crypto may be useful, especially when it allows them to access capital without selling an asset they want to keep.

The challenge is that understanding the concept is only one part of the decision.

Crypto-backed lending asks users to make a high-trust financial decision. Borrowers are not simply taking on credit. They are placing a valuable digital asset into a structure where interest rates, custody, collateral requirements, liquidation mechanics, platform risk, and regulatory uncertainty all matter.

For many prospective borrowers, that creates hesitation.

Among crypto holders who do not currently use a crypto-backed loan, the leading barriers were confidence-related. The most prominent concerns included managing crypto price volatility, managing liquidation risk, and uncertainty around crypto-backed loan regulation.

These are practical concerns. They suggest the category’s next phase of growth is likely to depend on making the product experience clearer, safer, and easier to trust.

Collateralized lending as a familiar financial behavior

One of the most important findings from the research is that crypto-backed lending is already understood through a familiar financial lens.

The study found that 72% of crypto holders agree crypto-backed loans provide convenient access to funds without needing to sell crypto.

That matters because the behavioural foundation is already there.

People understand the idea of keeping an asset while borrowing against it. This is deeply embedded in traditional finance. The newer part is applying the same logic to digital assets.

For crypto holders, the appeal is not simply “getting a loan.” It is the ability to preserve long-term exposure while accessing liquidity for another purpose.

That could mean funding a major purchase, managing cash flow, making an investment, or avoiding the need to sell crypto at a moment that does not align with their broader financial strategy.

The opportunity for crypto-backed lending is therefore not only about creating new financial products. It is about making a familiar financial behaviour feel credible and accessible in a newer asset class.

Building confidence infrastructure

At Protocol Theory, we think of this as a confidence infrastructure problem.

Confidence infrastructure refers to the product, communication, trust, and risk signals that help users feel safe enough to act.

For prospective borrowers, confidence is likely to mean several things:

- Clearer borrowing costs.

- Simple explanations of loan terms and risks.

- Greater visibility into liquidation mechanics.

- Reassurance that collateral is held safely.

- Trust in the platform’s track record and risk controls.

- Greater regulatory and operational clarity.

These factors matter because crypto-backed lending sits at the intersection of credit, custody, asset volatility, and platform trust.

That makes the decision more complex than many traditional consumer lending products. It also raises the standard for communication, transparency, and user experience.

For the category to scale, providers need to do more than communicate the abstract benefits of borrowing against crypto. They need to help users feel that the process is understandable, manageable, and safe enough to act on.

Borrowing behaviours across markets

The research also found meaningful directional differences between Australia and the United States.

Australian crypto holders were more likely than American crypto holders to borrow proactively as part of financial planning. They were also more likely to compare lenders across platforms before choosing.

This suggests Australia may currently be a more active provider-shopping environment for crypto-backed lending.

The United States, by comparison, appears to show a more measured borrowing posture. In a larger and more mature financial services market, trust-building and confidence may play an especially important role in conversion.

However, the broader story is consistent across both markets.

Crypto holders are open to borrowing. They can see the use case. But adoption depends on whether providers can reduce uncertainty and make borrowing against crypto feel more transparent, controlled, and trustworthy.

Closing crypto lending’s trust gap

The crypto borrowing gap is commercially significant because it points to latent demand that has not yet converted into widespread behaviour.

For crypto-backed lending providers, the implication is clear: growth is unlikely to come from demand generation alone.

The category needs stronger trust signals. More transparent product design. Clearer risk communication. Better borrower education. Stronger platform reassurance. Simpler explanations of what happens when crypto prices move, how liquidation thresholds work, and how collateral is protected.

Crypto-backed lending has the potential to bring a familiar financial behaviour into the digital asset market: borrowing against a long-term holding instead of selling it.

But that potential will depend on whether the category can close the confidence gap.

For Protocol Theory, the broader lesson is clear: in frontier financial categories, growth often depends less on awareness alone and more on whether providers can convert latent demand into confident behaviour.

The next phase of crypto-backed lending will be shaped by the providers that make borrowing feel less uncertain, more transparent, and more aligned with how people already think about long-term asset ownership.

◼️ Read Ledn’s original post on the research here, or download the full report below:

For more evidence-led perspectives on the future of money, technology, and digital markets, sign up to receive our latest insights.

About the research:

This article is based on research commissioned by Ledn and conducted by Protocol Theory. The study surveyed 1,244 cryptocurrency holders aged 18+ across the United States and Australia between February 19 and February 24, 2026, including 621 respondents in the United States and 623 respondents in Australia.

Related articles

Events & Webinars

Industry Insights